This is a listed company that attracts my attention. To keep it short, I would just share the reasons why I am attracted to it. More information about the group can be found at its

official website.

1. No offer for sale in IPO

The owners are not cashing out. Post IPO, the founders (husband and wife) are still very substantial shareholders, collectively holding 69.08% of the group. This is a good sign. It is likely that they will continue to work very hard for the group given their very significant stake in the group.

2. Competent and Experienced Management

The CEO and COO, husband and wife, have led the group for over 30 years. They brought in Ripley's Believe It Or Not Museum and Haunted Adventure to Genting Highland First World Hotel. Besides, the group runs 20 food outlets, 9 retail and other service outlets in Genting Highland. OWG is the largest 3rd party F&B operator in Genting Highland. Being able to be a significant partner at Genting Highland is a strong testimony of OWG's strength and competency.

And the Chairman and Group CEO Dato' Richard Koh is a veteran in the industry. He is:

i) The President of Asean Retail-Chains & Franchise Federation

ii) International Association of Amusement Park USA Board of Director & Asean Advisory

iii) Advisor of Malaysian Association of Amusement ThemePark & Family Attractions

3. Good margins

Skeptics are less impress that OWG's F&B brands are not so well-known. But when comparing with well-known brands such as Burger King Malaysia and A&W Malaysia which struggle with profitability, I would rather opt for margin. When analysing OWG, one has to understand that their business strategy is different from other F&B operators which adopt "scattered gun" approach. For these F&B players that have branches in shopping malls, brand awareness is important to attract patrons.

OWG services a captive market at Genting Highland and its theme parks that have sufficient attractions and activities to extend the visitors' stay in the areas. Visitors rarely go all the way to Genting mainly for the food there. But when visitors look for food in Genting, there is good chance of the visitors frequenting one of OWG's F&B outlets there.

When one visits a water theme park, the visitor has little choice but to purchase the food from the F&B outlets within the theme park. Brand is not so crucial here but how the operator retain visitors for longer stay at the theme park to increase their spending at the F&B outlets.

4. Expansion and Upgrading at Genting Highland

Genting Group is expanding the number of rooms at Genting Highland and upgrading the outdoor theme park. This should bode well to OWG.

5. Cash business

OWG's businesses are mainly cash business. So cash collection is not a major concern.

6. Net cash position

Based on the pro forma consolidated balance sheet, the group is expected to be in net cash position post ipo and utilisation of listing proceeds

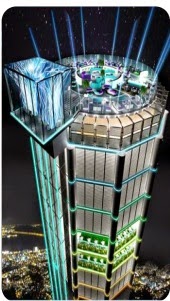

7. Low rental rate at Komtar

The rental rate for the 130,333sq ft of space at Komtar Penang for the

i) proposed multi-purpose hall and open air bazaar at 5th floor;

ii) high end international food service outlets, entertainment outlets and ballroom at 59th and 60th floor; and

iii) High end international food service outlets and lookout deck at 64th and 65th floor (rooftop)

is only RM0.69 psf.

2 exterior sky bubble lifts linking the 5th floor directly to 59th and 65th levels are intended to be installed to allow passengers riding in the sky lifts to experience distinctive bird's eye view of Georgetown and Penang.

I would say the Penang State Government has been successful in transforming Penang into a tourism hot spot. Some places of interest near Komtar includes street art and wall painting in Georgetown, Armenian Street Got Talent on every Saturday, Project Occupy Beach Street every Sunday, Chew Jetty, and various famous hawker food nearby. After Komtar is revitalised by OWG, it could potentially becomes a tourist hot spot.

At IPO price of 88sen/share, it is pegged at a historical PE ratio of 11x. Given the reason above, and potential significant growth from the Komtar revitalisation project, I think it deserves a higher target PE ratio.