Mr Koon Yew Yin blogged about Xingquan. Cash about RM3/share, EPS was 42sen/share for FY15, with PE multiple less than 2x.

If the share price does not reflect its true value, at current share price of 60sen/share, why not the major shareholder privatise the company?

If the major shareholder offers to privatise the company at RM2/share, not only he does not have to fork out money to take the company private, yet he actually earns RM1/share plus the remaining ownership of the company for free.

Is there such a big toad jumping on the street?

Added on 1 Jan 2016

Would you invest in a company that carries net cash of RM934m as of end September 2015 still needs rights issue to raise RM50.7m to fund RM99.2m capex?

Thursday 31 December 2015

Wednesday 30 December 2015

Open Letter to Ahmad Maslan

Dear Ahmad Maslan,

It is not easy to take two jobs, especially in Malaysia.

1. Traffic is too heavy on the road, especially during peak hours. This is aggravated by poor road conditions such as potholes, worn-off pavement surface. The situation is worse whenever there is heavy downpour. Some areas are flooded due to indiscriminate felling of tree for development. These make it difficult for people to rush for part-time jobs in the evening after their main jobs.

2. The Rakyat have limited choice but to own cars due to poor public transport system. Owning a car is quite burdensome for the lower income group. But even owning a car, one may still unable to reach his workplace in time for part-time job, as explained above.

3. Lack of car park space, especially at busy commercial areas could be a deterrent as well.

4. The Rakyat do not feel safe, more so at night. One may be a target when returning home late at night after part-time job. Not only his belongings but his life may be taken away together by robbers, snatch-thieves.

5. Lack of proper covered walkway in the cities makes it difficult for Rakyat to go to workplace. There are interchanges of railway lines still without all-weather protection walkway and seamless links between interchanges.

6. After the recent sharp toll hikes, the toll fare could eat into one’s hard-earned part-time wage. Bad news is that there will be more toll hikes in 2016, unless the government is willing to absorb the rate hikes.

Would you quickly get the government to address the above first so that taking second job is more possible?

Regards

One who is desperately looking for second job

It is not easy to take two jobs, especially in Malaysia.

1. Traffic is too heavy on the road, especially during peak hours. This is aggravated by poor road conditions such as potholes, worn-off pavement surface. The situation is worse whenever there is heavy downpour. Some areas are flooded due to indiscriminate felling of tree for development. These make it difficult for people to rush for part-time jobs in the evening after their main jobs.

2. The Rakyat have limited choice but to own cars due to poor public transport system. Owning a car is quite burdensome for the lower income group. But even owning a car, one may still unable to reach his workplace in time for part-time job, as explained above.

3. Lack of car park space, especially at busy commercial areas could be a deterrent as well.

4. The Rakyat do not feel safe, more so at night. One may be a target when returning home late at night after part-time job. Not only his belongings but his life may be taken away together by robbers, snatch-thieves.

5. Lack of proper covered walkway in the cities makes it difficult for Rakyat to go to workplace. There are interchanges of railway lines still without all-weather protection walkway and seamless links between interchanges.

6. After the recent sharp toll hikes, the toll fare could eat into one’s hard-earned part-time wage. Bad news is that there will be more toll hikes in 2016, unless the government is willing to absorb the rate hikes.

Would you quickly get the government to address the above first so that taking second job is more possible?

Regards

One who is desperately looking for second job

Saturday 26 December 2015

Teoseng - Forming of Head and Shoulders?

Unless it can break and stay above RM1.70, head and shoulders that is being formed in weekly and monthly charts may suggest more downside in the share price.

Weekly chart.

Weekly chart.

Monthly chart. Long upper shadow formed in the last 3 candles, pointing to bearish sign

Thursday 24 December 2015

Differing Views on Tomypak

I wrote about Tomypak in early October when the share price was RM2.39. It touched a high of RM3 on 18 Nov 15. The share price underwent correction and closed at RM2.64 on 23 Dec 15.

CIMB is the only broker covering Tomypak currently. While I am positive on the outlook of the company, CIMB was quite skeptical on the margin improvement and its expansion plan. It is alright to have differing opinions as long as the reasoning is sensible.

The 2 latest reports by CIMB (for registered users only) can be found here:

Running to far ahead dated 26 Nov 15

Over-ambitious 10-year capex strategy dated 13 Dec 15

1. Earnings beat expectation, higher dividend payout, raised earnings forecasts but cut target price

The first report dated 26 Nov 15 was 3Q15 results note. Tomypak reported:

i. net profit above CIMB's expectation

ii. profit margin recovery continues

iii. dividend payout for 9M improved from 4sen/share to 7sen/share

Subsequently, CIMB raise its FY15-17 EPS forecasts by 4-6% to reflect further profit margin recovery.

Despite the good set of results and earnings upgrade by the CIMB, the same broker surprisingly cut the target price from RM1.96 to RM1.84! It didn't seem to jibe. Perplexing...

2. Profit margin recovery mystery?

CIMB was perplexed by Tomypak's sharp profit margin recovery as the broker opined that operational improvements are usually in baby steps, not triple jumps. According to CIMB, both Daibochi and Tomypak have similar customers and, as such, profit margins from sales should be relatively similar.

From the same report, similar margin improvement could be observed in 2008 and EBITDA margin of slightly above 20% was also seen in early 2009. So this was not a margin that had not been seen before. Furthermore, the margin improvement came from a low base.

The broker was unsure how the company's profit margin recovered so quickly since the entry of a new major shareholder in 4Q14.

Mr. Lim Hun Swee was re-designated as an executive director in August 2014 and subsequently as a Managing Director on 1 January 2015. Mr. Lim Hun Swee is a veteran in the food industry. According to Bloomberg, he also served as an Executive at MNC Wireless Berhad, Hup Seng Industries Bhd., eBworx Bhd, OSK Holdings Bhd., HLG Capital Bhd, Global Soft Bhd, ISS Consulting Solutions Bhd. Mr. Lim served as Managing Director of In-Comix Food Industries Sdn. Bhd. until July 2009. He has 20 years experience. He has been a Non Independent Executive Director of Tomypak Holdings Bhd since August 13, 2014 and served as its Non Independent & Non Executive Director from May 23, 2014 to August 13, 2014. Mr. Lim has been an Executive Director of Johore Tin Bhd since July 1, 2012 and its Non Executive Director from August 26, 2010 to July 1, 2012.

Mr. Lim has been increasing his stake in Tomypak since he took over the executive role in Tomypak and this could be a sign of his confidence in the prospects of the company.

If the earnings were not real, how the group paid for RM12m land purchase, part of the capex for factory expansion and increased dividend payout?

3. Were the "facts" in the reports right?

Its report dated 26 Nov 15 stated the company geared up to finance the set-up of a new factory, which would double existing plant capacity.

In The Edge Weekly dated 20 July 2015, Tomypak is planning to build a new plant with an annual production capacity of 35,000 tonnes on 10.5 acres of industrial land in Senai, Johor. Its existng plant in Tampoi, Johor Bahru, which has a production capacity of 17,500 tonnes, is running at a utilisation rate of 80%. It should be tripling of capacity instead of doubling the capacity.

Separately in CIMB report dated 13 December 2015, it wrote in Phase 1, Tomypak hopes to double its production capacity by end-2016. The Edge Weekly dated 14 December 2015 (available 12 December 2015) highlighted Tomypak has a planned capex of RM120m to RM140m for its three-phase new factory project. Each phase will provide 12,000 tonnes of additional capacity per annum. It will be two-thirds increase in existing capacity instead of doubling capacity.

4. Expansion long overdue or overly ambitious?

But when Tomypak revealed its plan to triple its capacity in 10 years (at CAGR of 11.6%), the broker raised its doubt whether the expansion plan was overly ambitious.

While it is true that overseas MNC customers are very sticky and it could take a minimum of 2-3 years for them to switch suppliers, Tomypak could possibly secure additional orders from its existing MNC customers. Central procurement is common in MNCs. Tomypak which has significant revenue generated from overseas markets, may gain market share through its existing MNC clients. The additional orders from overseas markets could be very sizeable.

5. Imposed steep discount to a superior player?

Compared with Daibochi, Tomypak is superior in term of margin, ROE, ROA, lower gearing, better trading liquidity and growth potential. Not only a steep discount imposed on Tomypak's target PE multiple puzzling, CIMB widened the discount from 30% to 40% in its report dated 26 Nov 2015 when earnings beat expectation, margin continued to improve, and dividend payout increased was even more baffling!

CIMB is the only broker covering Tomypak currently. While I am positive on the outlook of the company, CIMB was quite skeptical on the margin improvement and its expansion plan. It is alright to have differing opinions as long as the reasoning is sensible.

The 2 latest reports by CIMB (for registered users only) can be found here:

Running to far ahead dated 26 Nov 15

Over-ambitious 10-year capex strategy dated 13 Dec 15

1. Earnings beat expectation, higher dividend payout, raised earnings forecasts but cut target price

The first report dated 26 Nov 15 was 3Q15 results note. Tomypak reported:

i. net profit above CIMB's expectation

ii. profit margin recovery continues

iii. dividend payout for 9M improved from 4sen/share to 7sen/share

Subsequently, CIMB raise its FY15-17 EPS forecasts by 4-6% to reflect further profit margin recovery.

Despite the good set of results and earnings upgrade by the CIMB, the same broker surprisingly cut the target price from RM1.96 to RM1.84! It didn't seem to jibe. Perplexing...

2. Profit margin recovery mystery?

CIMB was perplexed by Tomypak's sharp profit margin recovery as the broker opined that operational improvements are usually in baby steps, not triple jumps. According to CIMB, both Daibochi and Tomypak have similar customers and, as such, profit margins from sales should be relatively similar.

From the same report, similar margin improvement could be observed in 2008 and EBITDA margin of slightly above 20% was also seen in early 2009. So this was not a margin that had not been seen before. Furthermore, the margin improvement came from a low base.

The broker was unsure how the company's profit margin recovered so quickly since the entry of a new major shareholder in 4Q14.

Mr. Lim Hun Swee was re-designated as an executive director in August 2014 and subsequently as a Managing Director on 1 January 2015. Mr. Lim Hun Swee is a veteran in the food industry. According to Bloomberg, he also served as an Executive at MNC Wireless Berhad, Hup Seng Industries Bhd., eBworx Bhd, OSK Holdings Bhd., HLG Capital Bhd, Global Soft Bhd, ISS Consulting Solutions Bhd. Mr. Lim served as Managing Director of In-Comix Food Industries Sdn. Bhd. until July 2009. He has 20 years experience. He has been a Non Independent Executive Director of Tomypak Holdings Bhd since August 13, 2014 and served as its Non Independent & Non Executive Director from May 23, 2014 to August 13, 2014. Mr. Lim has been an Executive Director of Johore Tin Bhd since July 1, 2012 and its Non Executive Director from August 26, 2010 to July 1, 2012.

Mr. Lim has been increasing his stake in Tomypak since he took over the executive role in Tomypak and this could be a sign of his confidence in the prospects of the company.

If the earnings were not real, how the group paid for RM12m land purchase, part of the capex for factory expansion and increased dividend payout?

3. Were the "facts" in the reports right?

Its report dated 26 Nov 15 stated the company geared up to finance the set-up of a new factory, which would double existing plant capacity.

In The Edge Weekly dated 20 July 2015, Tomypak is planning to build a new plant with an annual production capacity of 35,000 tonnes on 10.5 acres of industrial land in Senai, Johor. Its existng plant in Tampoi, Johor Bahru, which has a production capacity of 17,500 tonnes, is running at a utilisation rate of 80%. It should be tripling of capacity instead of doubling the capacity.

Separately in CIMB report dated 13 December 2015, it wrote in Phase 1, Tomypak hopes to double its production capacity by end-2016. The Edge Weekly dated 14 December 2015 (available 12 December 2015) highlighted Tomypak has a planned capex of RM120m to RM140m for its three-phase new factory project. Each phase will provide 12,000 tonnes of additional capacity per annum. It will be two-thirds increase in existing capacity instead of doubling capacity.

4. Expansion long overdue or overly ambitious?

On expansion, CIMB in the report dated 26 Nov 15 commented the building of a new factory is a long overdue exercise as the existing factory has insufficient space, and added that Tomypak should have done this expansion a few years ago.

But when Tomypak revealed its plan to triple its capacity in 10 years (at CAGR of 11.6%), the broker raised its doubt whether the expansion plan was overly ambitious.

While it is true that overseas MNC customers are very sticky and it could take a minimum of 2-3 years for them to switch suppliers, Tomypak could possibly secure additional orders from its existing MNC customers. Central procurement is common in MNCs. Tomypak which has significant revenue generated from overseas markets, may gain market share through its existing MNC clients. The additional orders from overseas markets could be very sizeable.

5. Imposed steep discount to a superior player?

Compared with Daibochi, Tomypak is superior in term of margin, ROE, ROA, lower gearing, better trading liquidity and growth potential. Not only a steep discount imposed on Tomypak's target PE multiple puzzling, CIMB widened the discount from 30% to 40% in its report dated 26 Nov 2015 when earnings beat expectation, margin continued to improve, and dividend payout increased was even more baffling!

Friday 27 November 2015

Ann Joo is actually loss-making in 3Q15

Another listed company misreported its results on the summary page after Notion Vtec.

On the summary page, Ann Joo reported strong "gain" of RM82.3m.

But if you look into the income statement, Ann Joo was actually incurring substantial amount of loss!

Friday 20 November 2015

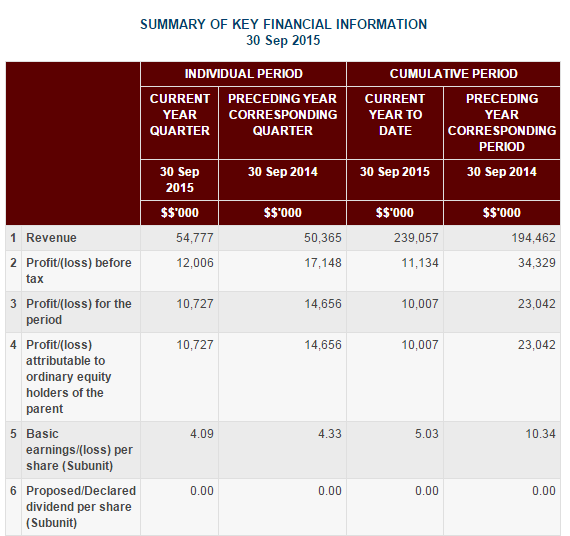

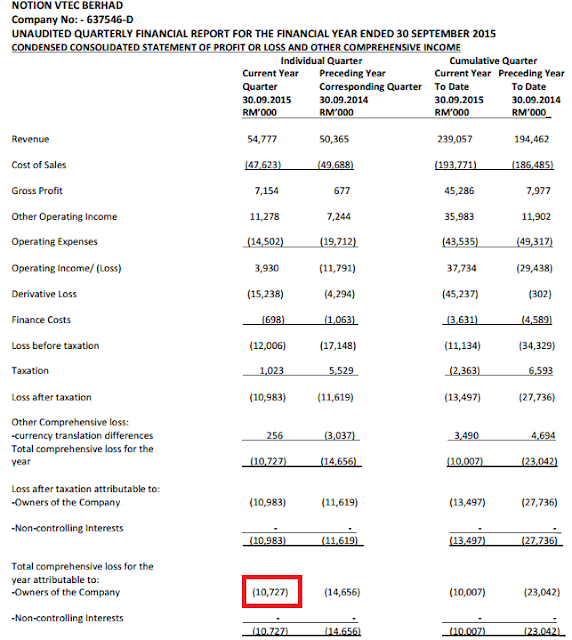

Questionable Notion Vtec

First, the missing negative sign in the results summary page makes a huge difference.

But, the misguidance by the management is actually more worrying. In the immediate preceding quarter, the company commented:

Bulk of the unfavourable forward contracts had expired. Things should improve from this quarter onwards right?

In the results released yesterday, the company recorded RM15.2m of derivative loss! Now the company said they still have exposure until May and September 2016???

It actually incurred a loss in 4QFY15!!

Bulk of the unfavourable forward contracts had expired. Things should improve from this quarter onwards right?

In the results released yesterday, the company recorded RM15.2m of derivative loss! Now the company said they still have exposure until May and September 2016???

Wednesday 28 October 2015

A company with "negative" cash position performed share buy back???

A listed company should buy back its own shares only when there is excess cash. However, there is a company that performed share buy back when its most recent quarter report showed it was in "negative" cash position.

(Source)

(Source)

Is this an appropriate time to do share buy back?

Is this an appropriate time to do share buy back?

Thursday 15 October 2015

Is Johotin due for sector reclassification?

Johotin is listed under industrial sector. I think it is more rightly to re-classify Johotin as a consumer products counter.

According to Paragraph 4.2 of Bursa's Practice Note 7 - Classification of applicants and listed issuers,

Johotin's F&B segment has overtaken its tin manufacturing division since 2012 and maintain a large gap between the two divisions.

2012

It could be a potential re-rating catalyst when the stock is reclassified into consumer products sector

According to Paragraph 4.2 of Bursa's Practice Note 7 - Classification of applicants and listed issuers,

In determining the Classification of the applicant or listed issuer into any one of the Sectors, an applicant or a listed issuer must examine the amount of contribution made by its various business activities for the past 2 years. A listed issuer will be classified into the Sector which most closely fits its source of revenue or if there are several sources of revenue, the business which consistently generates the highest revenue of the listed issuer. The Classification will also be determined based on either the immediate end use of the product or the industry processes used.

Johotin's F&B segment has overtaken its tin manufacturing division since 2012 and maintain a large gap between the two divisions.

2012

2013

2014

It could be a potential re-rating catalyst when the stock is reclassified into consumer products sector

Saturday 3 October 2015

Tomypak - Turning Over A New Leaf

Tomypak is in the business of flexible packaging. Its revenue derived from local market and overseas market is equally split.

Turning Over A New Leaf

To analyse Tomypak, one may consider segregating its financial performance before and after 1 January 2015, the point when new Managing Director Mr Lim Hun Swee took over the leadership of the company.

Tomypak's margin had actually surpassed that of Daibochi's, one of its closest local competitor, since 4Q14, after Mr. Lim Hun Swee was redesignated from a non-executive director in Tomypak to an executive director on 13 August 2014.

Without gross profit being disclosed by both companies in their quarterly results, no comparison could be made between their gross margin, distribution expenses and administrative expenses in FY15 until the release of their FY15 annual reports in 2Q16.

Peer Comparison

Except for bigger market cap and higher dividend policy, Tomypak is a clear winner. It is more efficient in term of operation (operating margin), asset utilisation (ROA), capital utilisation (ROE), having healthy balance sheet (net gearing), and possibly better growth potential as Tomypak is expanding its capacity. And yet, Tomypak's PE ratio is just almost half of Daibochi's

Right Price, Right Business, Right Management?

Price

Tomypak appears to fulfill the 3-Rights, right price, right business and right management, the 3 core criteria used by Yeoman Capital Management in stock selection.

Being a proxy to the F&B sector and being traded below 12 times PE multiple, the share price of Tomypak is undemanding compared with its closest local competitor, Daibochi, which being traded at about 19 times PE multiple, and other F&B companies. The undergoing plant expansion also provides growth potential.

Business

Flexible packaging is deemed to be a resilient business, especially when almost all of Tomypak's products are catered for F&B players. Its clients include:

The demand for F&B flexible packaging is expected to remain pretty stable despite uncertainties in the economic outlook.

Management

The turnaround in Tomypak's financial performance could be attributed to the change of stewardship since Mr. Lim Hun Swee took over the management of the company. Mr Lim is a veteran is the F&B sector. He set up In-Comix Food Industries Sdn Bhd in 1989 before disposing the company in 2009. Mr. Lim was previously employed as a Managing Director by Grand United Marketing Sdn. Bhd. and a Managing Director by Taste N Tasty Food Industries Sdn. Bhd. Currently, he is an executive director in Johotin which involves in F&B and can businesses. He is said to be instrumental in reviving Johotin which diversified into F&B business in 2011.

He has set an interesting target of overtaking its competitor Daibochi in term of market cap in 3 years time.

Mr Lim has 15.35% ownership in Tomypak (1 Oct 2015) whereas Mr Lim Soo Koon, Daibochi's Managing Director has only 0.16% ownership in Daibochi. Tomypak is closer to owner-management while Daibochi is run by a professional manager.

Target Price

Given the industry Tomypak is in, its financial ratio, peer comparison, growth prospect, trading at PE multiple of 12 times doesn't appear demanding.

I leave it to you to imagine the potential target price of Tomypak based on:

i) Reasonable PE multiple it should be traded at; and

ii) Its growth potential (whether it can secure sufficient orders after tripling its capacity)

iii) Whether margin could be maintained

Potential catalysts:

i) PE multiple re-rating

ii) Potential earnings growth from plant expansion

iii) Possible premium if Tomypak overtakes Daibochi to be local market leader in flexible packaging

Turning Over A New Leaf

To analyse Tomypak, one may consider segregating its financial performance before and after 1 January 2015, the point when new Managing Director Mr Lim Hun Swee took over the leadership of the company.

Tomypak's margin had actually surpassed that of Daibochi's, one of its closest local competitor, since 4Q14, after Mr. Lim Hun Swee was redesignated from a non-executive director in Tomypak to an executive director on 13 August 2014.

Margin (%) | Daibochi | Tomypak | Difference (% pts) |

4Q14 | |||

Operating | 8.17 | 9.17 | 1.00 |

PBT | 8.49 | 8.88 | 0.39 |

PATAMI | 7.03 | 7.38 | 0.35 |

1Q15 | |||

Operating | 9.05 | 14.78 | 5.73 |

PBT | 9.46 | 14.54 | 5.08 |

PATAMI | 7.18 | 10.22 | 3.04 |

2Q15 | |||

Operating | 10.71 | 15.95 | 5.24 |

PBT | 10.64 | 15.91 | 5.27 |

PATAMI | 8.02 | 11.69 | 3.67 |

Without gross profit being disclosed by both companies in their quarterly results, no comparison could be made between their gross margin, distribution expenses and administrative expenses in FY15 until the release of their FY15 annual reports in 2Q16.

Peer Comparison

Daibochi | Tomypak | Winner | |

Market Cap (RMm) | 506.6 | 261.6 | Daibochi |

1H15 Operating Margin (%) | 9.90 | 15.35 | Tomypak |

PE ratio (annualised FY15 earnings) | 18.9 | 11.7 | Tomypak |

Dividend Policy | 60% | 40% | Daibochi |

Dividend Yield (%) (annualised FY15 dividend) | 3.37 | 3.35 | On par |

ROA (%) (annualised FY15 earnings) | 8.95 | 12.99 | Tomypak |

ROE (%) (annualised FY15 earnings) | 15.59 | 19.34 | Tomypak |

Net Gearing (%) | 35.29 | 3.33 | Tomypak |

Capacity Expansion | ? (Existing production floor space 460k) | Tripling its capacity from 17,500MT to 52,500MT | Maybe Tomypak |

Utilisation rate | 60% | 80% | Tomypak |

Average daily share trading volume (for past 1 year) | 46.637k | 197.62k | Tomypak |

Except for bigger market cap and higher dividend policy, Tomypak is a clear winner. It is more efficient in term of operation (operating margin), asset utilisation (ROA), capital utilisation (ROE), having healthy balance sheet (net gearing), and possibly better growth potential as Tomypak is expanding its capacity. And yet, Tomypak's PE ratio is just almost half of Daibochi's

Right Price, Right Business, Right Management?

Price

Tomypak appears to fulfill the 3-Rights, right price, right business and right management, the 3 core criteria used by Yeoman Capital Management in stock selection.

Being a proxy to the F&B sector and being traded below 12 times PE multiple, the share price of Tomypak is undemanding compared with its closest local competitor, Daibochi, which being traded at about 19 times PE multiple, and other F&B companies. The undergoing plant expansion also provides growth potential.

Business

Flexible packaging is deemed to be a resilient business, especially when almost all of Tomypak's products are catered for F&B players. Its clients include:

The demand for F&B flexible packaging is expected to remain pretty stable despite uncertainties in the economic outlook.

Management

The turnaround in Tomypak's financial performance could be attributed to the change of stewardship since Mr. Lim Hun Swee took over the management of the company. Mr Lim is a veteran is the F&B sector. He set up In-Comix Food Industries Sdn Bhd in 1989 before disposing the company in 2009. Mr. Lim was previously employed as a Managing Director by Grand United Marketing Sdn. Bhd. and a Managing Director by Taste N Tasty Food Industries Sdn. Bhd. Currently, he is an executive director in Johotin which involves in F&B and can businesses. He is said to be instrumental in reviving Johotin which diversified into F&B business in 2011.

He has set an interesting target of overtaking its competitor Daibochi in term of market cap in 3 years time.

Mr Lim has 15.35% ownership in Tomypak (1 Oct 2015) whereas Mr Lim Soo Koon, Daibochi's Managing Director has only 0.16% ownership in Daibochi. Tomypak is closer to owner-management while Daibochi is run by a professional manager.

Target Price

Given the industry Tomypak is in, its financial ratio, peer comparison, growth prospect, trading at PE multiple of 12 times doesn't appear demanding.

I leave it to you to imagine the potential target price of Tomypak based on:

i) Reasonable PE multiple it should be traded at; and

ii) Its growth potential (whether it can secure sufficient orders after tripling its capacity)

iii) Whether margin could be maintained

Potential catalysts:

i) PE multiple re-rating

ii) Potential earnings growth from plant expansion

iii) Possible premium if Tomypak overtakes Daibochi to be local market leader in flexible packaging

Wednesday 19 August 2015

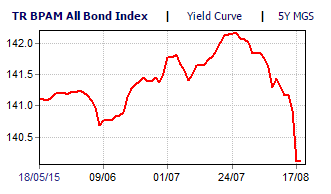

Are you still speculating on property?

Where are we now? Probably somewhere at 2 to 4 o'clock

The prices of major asset classes have declined.

Stock market has come down

Price of local bonds have come down

Gold price had started to decline much earlier

Crude oil, Brent, has started to plunge since end-2014

And RM is not spared, returning to 1998 financial crisis level

Prices of major asset classes have dropped. Prices of property stay elevated. Do you see 6 o'clock coming?

Tuesday 11 August 2015

Wednesday 22 July 2015

Bursa is still upgrading its announcement dissemination system

Bursa replaced its announcement dissemination system in April. Announcements for a period of 5 years from 1 January 2010 were made available on the website and the remaining past announcements on Bursa Malaysia website were supposed to be progressively increased to 15 years within 3 months from 20 April 2015, i.e. 20 July 2015.

Hiccup in system upgrade is not uncommon. But being the operator of stock exchange with market capitalisatin of more than RM1 trillion, the person-in-charge should at least update the revised expected completion date/ status of the system upgrade. Where is the accountability?

Wednesday 17 June 2015

Hevea: Directors' Remuneration - Why non-executive director's remuneration so much higher than executive director?

Below is the directors' remuneration for FY13 and FY14

Why was the non-executive director getting RM1.45m to RM1.5m in FY14 and RM1.4m to RM1.45m in FY13, roughly double the remuneration of the highest paid executive director?

Why was the non-executive director getting RM1.45m to RM1.5m in FY14 and RM1.4m to RM1.45m in FY13, roughly double the remuneration of the highest paid executive director?

Shareholders who attend the agm this Friday may want to find this out from the board of directors.

Shareholders who attend the agm this Friday may want to find this out from the board of directors.

Thursday 11 June 2015

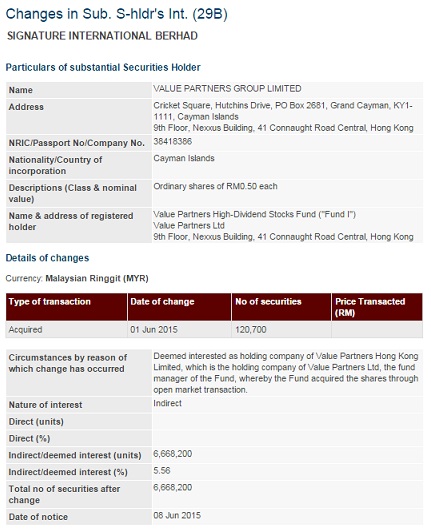

Cheah Cheng Hye vs Tan Teng Boo in Signature International Berhad

Two big surprises here

1. Value partners Group which has assets under management (AUM) of US$17b emerged as a substantial shareholder in Signature International Berhad, a smallcap in Bursa Malaysia with market cap of RM333.6m

2. Melting signs versus value. Both Cheah Cheng Hye and Tan Teng Boo are proponents of value investing. However, both of them have contradicting views on Signature.

Cheah Cheng Hye was awarded the Best of the Best Region Awards -CIO of the Year in Asia in 2011, was named 25 most influential people in Asian Hedge Funds in 2010, and 25 most influential people in asset management in Asia in 2009. Cheah Cheng Hye has been given the nicknames by the Chinese media including Golden Finger and Warren Buffett of the East.

Cheah Cheng Hye outperforms Tan Teng Boo in term of AUM and awards received. However, I think Tan Teng Boo is a better salesman, and stronger in marketing, but a bit arrogant and manipulative at times.

It will be interesting to see who makes the right call on Signature. However, Tan Teng Boo probably has lost the first round. He alerted the audience on the melting signs in Signature during his seminar on 9 May 2015. Despite the FBMKLCI has dropped 4.0% since the seminar, Signature has gained 18.3% since then, an out-performance of 22.3 in a month's time! A disastrous call on Signature by Tan Teng Boo

Thursday 4 June 2015

Asia Media: How much the worth of the board of directors' trustworthiness?

Wrote about Asia Media and raised the question whether the board members of Asia Media performed their duties diligently.

RM(m)

|

1Q14

|

2Q14

|

3Q14

|

4Q14

|

1Q15

|

Revenue

|

6.873

|

4.898

|

4.760

|

4.363

|

3.555

|

PBT

|

0.282

|

-1.999

|

-2.362

|

-14.995

|

-5.52

|

PATAMI

|

0.327

|

-1.997

|

-2.362

|

-16.32

|

-5.575

|

In the latest quarterly results, while the revenue has been declining since 1Q14, when commenting of the groups prospects, the board maintained the same comment made since 1Q14 that "based on the above and barring any unforeseen circumstances, the Board of Directors is of the opinion that the prospects for the Group for the next quarter will remain favourable due to increasing customers' demand"

How could revenue keep declining when there is increasing customers' demand?

Who are the board members?

1. Datuk Seri Syed Ali Bin Tan Sri Abbas Alhabshee

2. Dato' Wong Shee Kai

3. Yeong Siew Lee (Senior Independent Non-Executive Director, redesignated on 13 Feb 2015)

4. Paul Jong Jun Hian (Appointed on 10 Feb 2015)

5. Dato' Hussain @ Rizal Bin A. Rahman (Resigned on 10 Feb 2015)

The chairman's statement by Datuk Seri Syed Ali Bin Tan Sri Abbas Alhabshee in 2014 annual report is not less amazing...

"2014 was a strong year, due to existing customers demand and an influx of new customers. As a result of the good performance of the multimedia advertising services and media communication services in all three business segments, the Group presented another strong financial result in 2014. The Group reported its Revenue at RM20.89 million in FYE 2014, which achieved a CAGR of 29.07% since FYE 2007. Whilst our revenue FYE 2014 fell short of expectations which 40% lower as compare to last year, we are upbeat heading into 2015. The Group reported its EBITA of RM1.1million and net loss of RM20.5million in FYE 2014, caused by non-cash depreciation and amortisation expenses approximately RM28 million

How could it be a strong year when the revenue plunged 40% compared to a year ago and making substantial loss?

Excluding depreciation and amortisation expenses, the group was still loss-making at PBT level.

And how the Chairman obtained depreciation and amortisation expenses of approximately RM28m?

Amortisation of development costs RM22,966

Amortisation of intangible assets RM236,775

Depreciation of PPE RM20,366,854

Total: RM20,626,595

How low can the Datuk Chairman and board members go? What is the worth of their trustworthiness?

How could revenue keep declining when there is increasing customers' demand?

Who are the board members?

1. Datuk Seri Syed Ali Bin Tan Sri Abbas Alhabshee

2. Dato' Wong Shee Kai

3. Yeong Siew Lee (Senior Independent Non-Executive Director, redesignated on 13 Feb 2015)

4. Paul Jong Jun Hian (Appointed on 10 Feb 2015)

5. Dato' Hussain @ Rizal Bin A. Rahman (Resigned on 10 Feb 2015)

The chairman's statement by Datuk Seri Syed Ali Bin Tan Sri Abbas Alhabshee in 2014 annual report is not less amazing...

"2014 was a strong year, due to existing customers demand and an influx of new customers. As a result of the good performance of the multimedia advertising services and media communication services in all three business segments, the Group presented another strong financial result in 2014. The Group reported its Revenue at RM20.89 million in FYE 2014, which achieved a CAGR of 29.07% since FYE 2007. Whilst our revenue FYE 2014 fell short of expectations which 40% lower as compare to last year, we are upbeat heading into 2015. The Group reported its EBITA of RM1.1million and net loss of RM20.5million in FYE 2014, caused by non-cash depreciation and amortisation expenses approximately RM28 million

How could it be a strong year when the revenue plunged 40% compared to a year ago and making substantial loss?

Excluding depreciation and amortisation expenses, the group was still loss-making at PBT level.

And how the Chairman obtained depreciation and amortisation expenses of approximately RM28m?

Amortisation of development costs RM22,966

Amortisation of intangible assets RM236,775

Depreciation of PPE RM20,366,854

Total: RM20,626,595

How low can the Datuk Chairman and board members go? What is the worth of their trustworthiness?

Subscribe to:

Posts (Atom)