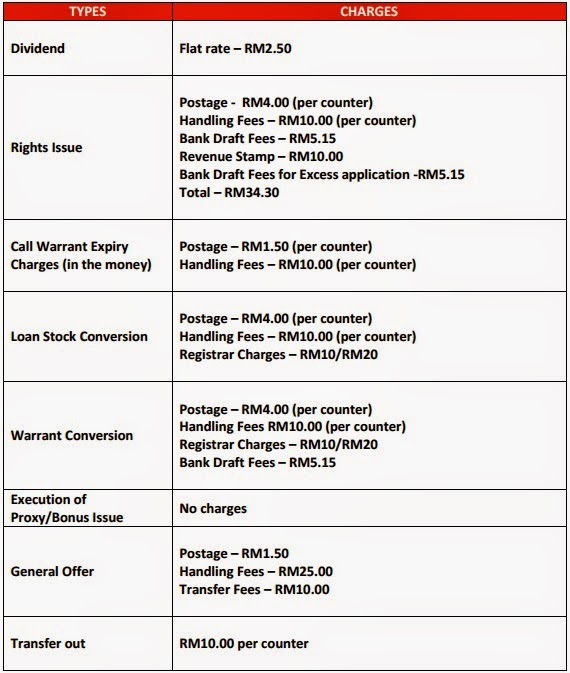

Corporate Exercise Fees for Nominess Account

|

State

|

Hectare

|

%

|

|

Johor

|

730,694

|

13.9

|

|

Kedah

|

85,182

|

1.6

|

|

Kelantan

|

140,035

|

2.6

|

|

Malacca

|

52,704

|

1.0

|

|

Negri Sembilan

|

170,048

|

3.2

|

|

Pahang

|

710,195

|

13.5

|

|

Perak

|

384,594

|

7.3

|

|

Perlis

|

278

|

0.01

|

|

Penang

|

13,480

|

0.2

|

|

Selangor

|

137,003

|

2.6

|

|

Terengganu

|

169,520

|

3.2

|

|

Peninsular Malaysia

|

2,593,733

|

49.6

|

|

Sabah

|

1,475,108

|

28.2

|

|

Sarawak

|

1,160,898

|

22.2

|

|

East Malaysia

|

2,636,006

|

50.4

|

|

TOTAL

|

5,229,739

|

|

|

|

COMPANY

|

RECORD

TITLE

|

|

1

|

7-Eleven Malaysia Sdn Bhd

|

Largest Convenience Chain Store

|

|

2

|

Bonia Corporation Bhd

|

Largest Leather Store Chain

|

|

3

|

Clara International

|

Largest Beauty Centre

|

|

4

|

Fitness Concept Specialist Chain Sdn

Bhd

|

Largest Fitness Specialist Chain Store

|

|

5

|

Focus Point Holdings Berhad

|

Largest Optical Chain Store

|

|

6

|

Golden Scoop Sdn Bhd

|

Largest Ice Cream Specialty Chain Store

|

|

7

|

King’s Confectionary Sdn Bhd

|

Largest Confectionary Chain Store

|

|

8

|

Kopitiam Asia Pacific Sdn Bhd

|

Largest Kopitiam Chain

|

|

9

|

Modern Mum Sdn Bhd

|

Largest Maternity Boutique Chain

|

|

10

|

Nelson’s Franchise (M) Sdn Bhd

|

Largest Corn In A Cup Franchise Outlet

|

|

11

|

OSIM (M) Sdn Bhd

|

Largest Healthcheck & Care

Equipment Chain

|

|

12

|

Pets More Sdn Bhd

|

Largest Pets Chain Store

|

|

13

|

Poh Kong Holdings Berhad

|

Largest Jewellery Retail Chain

|

|

14

|

Popular Book Co (M) Sdn Bhd

|

Largest Bookstore Chain

|

|

15

|

Secret Recipe Cakes & Cafe Sdn Bhd

|

Largest Cafe Chain

|

|

16

|

Senheng Electric (KL) Sdn Bhd

|

Largest Electrical Outlet Chain

|

|

17

|

Sinma Jewellery Centre Sdn Bhd

|

Largest Costume Jewellery Retail Chain

|

|

18

|

Sushi Kin Sdn Bhd

|

Largest Sushi Restaurant Chain

|

|

19

|

Thai Odyssey Sdn Bhd

|

Largest Thai Spa Operator

|

|

20

|

Urban Idea Sdn Bhd

|

Largest Sandwich Chain

|

|

21

|

Chatime

|

Largest Pearl Milk Tea Beverage Chain

|

|

22

|

BMS Organic

|

Largest Organic Retail Chain

|

|

23

|

Eu Yan Sang Sdn Bhd

|

Largest Herbs & Healthcare Retail

Chain

|