Just across the causeway...

Our first MRT will be ready by end 2016 (first section), when Singapore had their first in 1987, about 29 years ahead of us. We have been busy building more and more highways in the Klang Valley but Singapore concentrated on efficient public transport system.

Another big issue with the tolled highways is in order to keep the toll rates affordable, the government is compensating the toll concessionaires hundreds of millions every day, and the amount is increasing year by year. Not fair to those taxpayers who do not/ seldom use the tolled roads but having to subsidize others

Separately, Malaysia government is introducing gateless gantry toll system in 2018. Singapore had it 20 years ago, way back in 1988.

Why?

Thursday 30 April 2015

Thursday 16 April 2015

Bursa Malaysia Dynamic Price Limit

Subsequent to my posting about Bursa Malaysia Dynamic Price Limits, a reader, snowrain_berry has asked for more details about the dynamic price limits by Bursa Malaysia.

The details could be found here. Not sure if it is an official copy as I see yellow highlights in the manual, but the copy is from Bursa's website.

The details could be found here. Not sure if it is an official copy as I see yellow highlights in the manual, but the copy is from Bursa's website.

Golden Finger - Mr Lim Pei Tiam

Wrote about accumulation of Poh Huat shares by Mr Lim Pei Tiam in my previous posting in early Nov 14. The share price has almost doubled since then.

Then Mr Lim accumulated more shares in Super Enterprise in 1Q15 (see bursa announcement). The share price shot up late March 2015.

Khee San announced his substantial holdings (>5%) in Khee San yesterday. The share price gapped up this morning.

Then Mr Lim accumulated more shares in Super Enterprise in 1Q15 (see bursa announcement). The share price shot up late March 2015.

Khee San announced his substantial holdings (>5%) in Khee San yesterday. The share price gapped up this morning.

Wednesday 15 April 2015

Was Mr Tan Teng Boo extreme in his forecasts?

I know this is on hindsight, and I know it is hard to predict the time the market correctly.

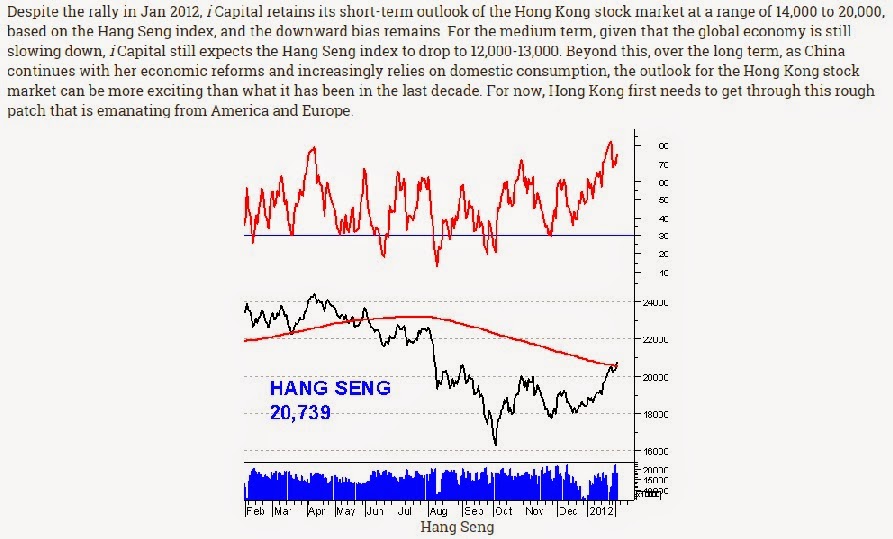

In Mr. Tan's newsletter dated 3 Feb 2012, he expects the Hang Seng Index to drop to 12,000-13,000. This was when the index was at 20,739 and it just crossed the moving average line, signaling a reversal from a bearish trend to a bullish one.

There was a mild correction in May 2012 but the index headed North since then. It did not drop below the low of about 16,170 recorded in Oct 2011, more so to the level of 12,000 and 13,000 predicted by Mr. Tan Teng Boo.

In his newsletter dated 4 April 2015, just eleven days ago, he retains his bearish outlook of the Hang Seng Index at a range of 15,000 to 23,000 in medium term. Taking the mid point of 19,000, that's about 25% downside from the closing of 15,275.

No prize for guessing the Hang Seng Index closing today. The index jumped about 9.3% in just 6 trading days. Mind you, a 9,3% jump in index is actually very significant. It was a surge of almost 11% if we compare to the highest close of the week at 28,016 recorded on 13 April 2015.

His I Capital International Value Fund has underperformed both benchmarks.

The Outperformance of his I Capital Global Fund against the benchmark has been narrowing since early 2014.

His Icapital.biz failed to impress as well. See previous postings:

What if you jumped into Icapital.biz after attending Investor Days?

Icapital.biz's return the bottom 20% in the past 5 years?

Does Icapital.biz outperform Berkshire Hathaway Inc.?

In his recent newsletter, he retains his bearish stance on FBMKLCI with a possibile target range of 800-900 for medium term. He still expects the KLCI to drop below 1,000 points before reversing.

Why such an extremist in the index predictions? Is there any structural change in the equity markets that he failed to notice?

I remember he advised investors not to time the markets but to invest in stocks with good prospects, right management, at undervalued share price as it would to futile to forecast the unpredictable market movement. But by keeping such a high level of cash in his fund and with such a bearish index forecast, is he timing the market?

He also advised investors not to listen to noise in the market. But, wasn't he emitting noise into the market by telling lots of "ghost stories" (frightening investors) for some time?

In Mr. Tan's newsletter dated 3 Feb 2012, he expects the Hang Seng Index to drop to 12,000-13,000. This was when the index was at 20,739 and it just crossed the moving average line, signaling a reversal from a bearish trend to a bullish one.

There was a mild correction in May 2012 but the index headed North since then. It did not drop below the low of about 16,170 recorded in Oct 2011, more so to the level of 12,000 and 13,000 predicted by Mr. Tan Teng Boo.

In his newsletter dated 4 April 2015, just eleven days ago, he retains his bearish outlook of the Hang Seng Index at a range of 15,000 to 23,000 in medium term. Taking the mid point of 19,000, that's about 25% downside from the closing of 15,275.

No prize for guessing the Hang Seng Index closing today. The index jumped about 9.3% in just 6 trading days. Mind you, a 9,3% jump in index is actually very significant. It was a surge of almost 11% if we compare to the highest close of the week at 28,016 recorded on 13 April 2015.

His I Capital International Value Fund has underperformed both benchmarks.

The Outperformance of his I Capital Global Fund against the benchmark has been narrowing since early 2014.

His Icapital.biz failed to impress as well. See previous postings:

What if you jumped into Icapital.biz after attending Investor Days?

Icapital.biz's return the bottom 20% in the past 5 years?

Does Icapital.biz outperform Berkshire Hathaway Inc.?

In his recent newsletter, he retains his bearish stance on FBMKLCI with a possibile target range of 800-900 for medium term. He still expects the KLCI to drop below 1,000 points before reversing.

Why such an extremist in the index predictions? Is there any structural change in the equity markets that he failed to notice?

I remember he advised investors not to time the markets but to invest in stocks with good prospects, right management, at undervalued share price as it would to futile to forecast the unpredictable market movement. But by keeping such a high level of cash in his fund and with such a bearish index forecast, is he timing the market?

He also advised investors not to listen to noise in the market. But, wasn't he emitting noise into the market by telling lots of "ghost stories" (frightening investors) for some time?

Monday 6 April 2015

Malakoff IPO - Project delay can be insured?

Paragraph 7.6.4.6 of Malakoff Draft Prospectus

"The EPC contractors for the construction of the Tanjung Bin Energy Power Plant have reported to us that, as at the Latest Practicable Date, the actual physical completion stood at approximately 79%, against the scheduled completion of approximately 88% resulting in a variance of approximately 9% in the construction progress due to civil engineering works at the plant site. Plans are currently being developed by the EPC contractors to reduce this variance. The civil engineering works related to the plant have now been substantially completed, and we believe that the variance will be further reduced. We expect to make an insurance claim with respect to any delay in achieving the plant's commercial operation date and expect that the insurance proceeds will substantially mitigate any claims under the TBE PPA."

Two common insurances that are taken up to cover risks in engineering projects are:

i) Contractor's All Risks; and

ii) Workmen's Compensation

If potential delay in a construction project can be insured, then life would be much easier for clients and contractors. But does such insurance covering project delay exist? If so, the controversy on LAD for the delay in completion of KLIA2 could have been avoided, and the risk of delay in completion of MRT project needs not be shouldered by Project Delivery Partner, as it could be transferred to insurance company.

But in actual, is life so easy for the contractors?

"The EPC contractors for the construction of the Tanjung Bin Energy Power Plant have reported to us that, as at the Latest Practicable Date, the actual physical completion stood at approximately 79%, against the scheduled completion of approximately 88% resulting in a variance of approximately 9% in the construction progress due to civil engineering works at the plant site. Plans are currently being developed by the EPC contractors to reduce this variance. The civil engineering works related to the plant have now been substantially completed, and we believe that the variance will be further reduced. We expect to make an insurance claim with respect to any delay in achieving the plant's commercial operation date and expect that the insurance proceeds will substantially mitigate any claims under the TBE PPA."

Two common insurances that are taken up to cover risks in engineering projects are:

i) Contractor's All Risks; and

ii) Workmen's Compensation

If potential delay in a construction project can be insured, then life would be much easier for clients and contractors. But does such insurance covering project delay exist? If so, the controversy on LAD for the delay in completion of KLIA2 could have been avoided, and the risk of delay in completion of MRT project needs not be shouldered by Project Delivery Partner, as it could be transferred to insurance company.

But in actual, is life so easy for the contractors?

Saturday 4 April 2015

What if you jumped into Icapital.biz after attending Investor Days?

These are the results versus KLCI performance if you have jumped into icapital,biz immediate after attending its Investor Days.

*adjusted for 9.5sen/share special dividend

Regardless whether it was the inaugural, second, third or the most recent investor day, your investment in Icapital.biz actually UNDER-PERFORMED FBMKLCI.

Note that adjustment has been made for 9.5sen/share special dividend that went ex in September 2013. The fund's performance is worse if you did not/ not entitled to claim back partial/full tax credit.

Wednesday 1 April 2015

Puzzling Pan Borneo Highway

Prime Minister launched the first phase of Pan Borneo Highway and said that the Sarawak portion will be toll-free.

According to an earlier report,

Transparency PLEASE!!!

Also in the article, it is also interesting to note that:

According to an earlier report,

The RM27 billion Pan Borneo Highway project is not a privatised project but comes under the Private Funding Initiative (PFI) where the company awarded the project will have to raise the necessary funds to construct the road first.

"I was made to understand that it is a PFI, though at the end of the day the Government will pay back the company," said Rural and Regional Development Minister, Datuk Seri Shafie Apdal.

The only difference compared to the PFI road projects in Semenanjung, he said, was that there would be no toll in Sabah.Why let the private company raise fund and pay them back later? The borrowing cost is unlikely to be cheaper than government's borrowing cost.

Transparency PLEASE!!!

Also in the article, it is also interesting to note that:

Fellow opposition Sabah Star head Datuk Dr Jeffrey Kitingan also said the Sabah government should insist that the Sabah section of the highway be built without any Malayan companies as the main contractor to avoid skimming of the contract sum and ending up with lower quality roads. "It should learn from the Sarawak road quality experience," he said. "No Malayan Umno companies or cronies are involved in the Sarawak section, he said: "If one were to take a leisurely drive in Lawas, Sarawak, some 850km from Kuching, one would notice that the roads in Lawas are wider by two feet and of better quality than those in Sabah. "Not only are Sabah roads narrower, they are full of potholes even in Kota Kinabalu."

He said the roads in Sabah were of poor quality due to the practice of sub-contract over sub-contract of the project, which resulted in many being forced to cut corners due to low prices.

"In Sarawak, they do not allow Umno-linked companies to be involved and due to the non-skimming at the top, there are better prices for Sarawak contractors," he said.

"It was not surprising and wise of the Sarawak government to name Lebuhraya Borneo Utara Sdn. Bhd to undertake the Sarawak portion of the Pan Borneo Highway and to reject any involvement by the Malayan Umno-linked companies," he said.

"Regardless whether they are from Umno or not, the Sabah government should adopt a similar stand to reject any Malayan company involvement in the Sabah Pan-Borneo Highway, to ensure Sabah contractors benefit from the construction and to prevent skimming of the contract sums.

Subscribe to:

Posts (Atom)